Tax Strategies

We’ll work with you to develop a tax minimization strategy.

Determining your current and future tax liability and developing a strategy that minimizes how much you pay during retirement is one part of building a retirement strategy. Taxes can impact your legacy and the assets you’ll be able to transfer to your heirs and beneficiaries. We recommend taking steps to help ensure that you’re taking advantage of any possible tax minimization strategies to help maintain the retirement you’ve worked hard to build.

A well-rounded retirement plan includes advanced tax strategies to reduce liabilities. Our expert tax planning services include:

Evaluating Current Holdings

Thorough assessment of the taxable nature of your current assets. Along with legal tax reduction strategies.

Incorporating Tax-Advantaged Investments

Strategically including taxed later or tax-free money in your portfolio. Along with tax loss harvesting.

Tax-Efficient Income Distribution

Developing a strategy for drawing income from the most beneficial tax categories first.

Tax-Free Legacy Planning

Exploring ways to use taxed later or taxed now funds to provide tax-free dollars to your beneficiaries.

Gains Harvesting

Tax-gain harvesting is its sophisticated (and often overlooked) sibling to tax-loss harvesting. Essentially, it is the practice of selling an investment that has increased in value to intentionally trigger a capital gain, then immediately buying it back (or buying something similar)

And over 1700 more different and effective tax planning strategies that we use for the families we work with to help them minimize taxes.

Tax Preparation vs. Tax Planning

We want you to pay your fair share of taxes and that is American, however we don’t want you to TIP the IRS. Pathways Retirement Advisors has a tax office that does Tax Preparation for clients of the Pathways Family. We do Tax Planning for all of our clients big or small. Tax Planning is not Tax Preparation.

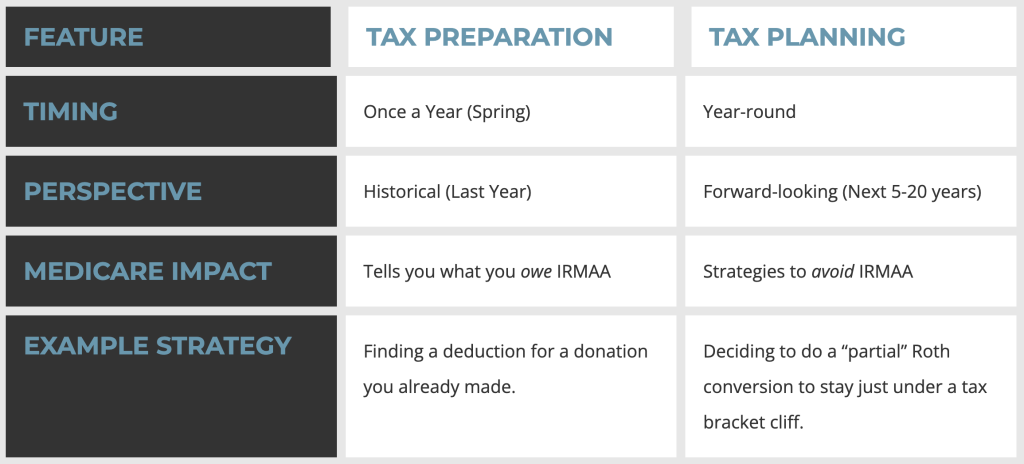

To put it simply: Tax preparation is looking in the rearview mirror, while tax planning is looking through the windshield.

While most people use the terms interchangeably, they represent two completely different approaches to your money. Understanding the difference is especially critical for retirees because of the “hidden” taxes like IRMAA.

Tax Preparation (Reactive)

Tax preparation is the process of documenting what has already happened. It is seasonal, typically occurring between January and April.

• The Goal: Accuracy and compliance. You want to make sure the IRS gets the right numbers and that you don’t get audited.

• The Focus: The past year. You gather your W-2s, 1099s, and receipts from last year and give them to a preparer to file a return.

• The Limitation: By the time you sit down with a tax preparer in March, there is very little you can do to change what you owe for the previous year. The “books are closed.”

Tax Planning (Proactive)

Tax planning is an ongoing, year-round strategy designed to minimize the amount of tax you pay over your entire lifetime, not just this year.

• The Goal: Efficiency and wealth preservation. It’s about choosing moves now that will lower your tax bill later.

• The Focus: The future. It involves analyzing different scenarios (like Roth conversions or the “gains harvesting”) before the year ends.

• The Strategic Edge: It coordinates your taxes with other parts of your life—like your Medicare premiums.

Feature

Tax Preparation

Tax Planning

Timing

Once a Year (Spring)

Year-round

Perspective

Historical (Last Year)

Forward-looking (Next 5-20 years)

Medicare Impact

Tells you what you owe IRMAA

Strategies to avoid IRMAA

Example Strategy

Finding a deduction for a donation you already made.

Deciding to do a “partial” Roth conversion to stay just under a tax bracket cliff.